Hello,

Guest!

Axis Bank MY ZONE Credit Card

Axis Bank SELECT Credit Card

IndianOil Axis Bank Credit Card

Axis Bank Magnus Credit Card

Flipkart Axis Bank Credit Card

Axis Bank Vistara Credit Card

Axis Bank Rewards Credit Card

Axis Bank Vistara Infinite Credit Card

Axis Bank Neo Credit Card

Samsung Axis Bank Signature Credit Card

Axis Bank Aura Credit Card

Axis Bank Kwik Rupay Credit Card

Axis Bank Vistara Signature Credit Card

Axis Bank Privilege Credit Card

Samsung Axis Bank Infinite Credit Card

Axis Bank Reserve Credit Card

Axis Bank Airtel Credit Card

Axis Bank Insta Easy Credit Card

Axis Bank Freecharge Credit Card

Axis Bank Forex Card

Axis Bank Rupay Credit Card

Axis Bank Burgundy Private Credit Card

Axis Bank Credit Card Interest Rates

Axis Bank Credit Card Pin Generation

Axis Bank Credit Card Offers

Axis Bank Credit Card Types

HDFC Freedom Credit Card

HDFC Indian Oil Credit Card

HDFC MoneyBack Credit Card

HDFC Infinia Credit Card

HDFC Diners Club Black Credit Card

HDFC Swiggy Credit Card

HDFC Regalia Credit Card

HDFC Millennia Credit Card

HDFC Business MoneyBack Credit Card

HDFC Regalia Gold Credit Card

HDFC Regalia First Credit Card

HDFC UPI Rupay Credit Card

Paytm HDFC Bank Credit Card

HDFC MoneyBack+ Credit Card

Tata Neu Plus HDFC Bank Credit Card

Shoppers Stop HDFC Bank Credit Card

Flipkart Wholesale HDFC Bank Credit Card

6E Rewards IndiGo Credit Card

HDFC Times Platinum Credit Card

HDFC Bank Corporate Platinum Credit Card

HDFC Rupay Credit Cards

HDFC Forex Cards

HDFC Virtual Credit Card

Best HDFC Credit Cards

Standard Chartered Smart Credit Card

Standard Chartered Manhattan Platinum Credit Card

Standard Chartered Platinum Rewards Credit Card

Standard Chartered EaseMyTrip Credit Card

Standard Chartered Credit Card Login

Standard Chartered Credit Card Customer Care

Standard Chartered Credit Card Bill Payment

Standard Chartered Bank Credit Card Statement

Instant Personal Loan Apps

Personal Loan Interest Rates

Zype Loan

Lendingplate Personal Loan

Unity Small Finance Personal Loan

SBI Personal Loan

HDFC Personal Loan

IDFC Personal Loan

Poonawalla Fincorp Personal Loan

Prefr Personal Loan

KreditBee Personal Loan

SmartCoin Personal Loan

Kotak Personal Loan

Bajaj Finserv Personal Loan

Tata Capital Personal Loan

Yes Bank Personal Loan

L&T Finance Personal Loan

Cashe Personal Loan

FlexiLoans Business Loan

KreditBee Business Loan

Prefr Credit Business Loan

LendingKart Business Loan

Protium Business Loan

IIFL Business Loan

NeoGrowth Business Loan

SBI Business Loan

ICICI Bank Business Loan

Bajaj Finserv Business Loan

HDFC Bank Business Loan

Axis Bank Business Loan

Women Business Loans

Unsecured Business Loans

Working Capital Loan

CGTMSE Scheme

MSME Loan

PSB Loans in 59 Minutes

SBI E Mudra Loan

PMEGP Loan

Mudra Loan

Startup Business Loan

Saksham Yuva Yojana

Pradhan Mantri Rojgar Yojana

PMFME Loan

PM Vishwakarma Yojana

Home Loan Interest Rates

Best Home Loan Interest Rates

HDFC Home Loan

DDA Housing Scheme 2025

PNB Housing Finance

Tata Capital Housing Finance

Aditya Birla Housing Finance

Kotak Mahindra Bank Home Loan

IDFC First Home Loan

Bajaj Finserv Home Loan

5 Crore Home Loan EMI

2 Crore Home Loan EMI

1 Crore Home Loan EMI

70 Lakh Home Loan EMI

Pradhan Mantri Awas Yojana

Hero Housing Finance

Home Loan Balance Transfer Interest Rates

HDFC Home Loan Balance Transfer

Kotak Home Loan Balance Transfer

PNB Home Loan Balance Transfer

Home First Home Loan Balance Transfer

Canara Bank Home Loan Balance Transfer

PNB Housing Finance Home Loan Balance Transfer

Aditya Birla Housing Finance Home Loan Balance Transfer

Loan Against Property Interest Rate

TCHFL Loan Against Property

Muthoot Fincorp Loan Against Property

HDFC Loan Against Property

Federal Bank Loan Against Property

Aditya Birla Housing Finance

Kotak Loan Against Property

IDFC First Loan Against Property

Home First Loan Against Property

SBI Loan Against Property

PNB Housing Loan Against Property

Bajaj Finance Loan Against Property

Loan Against Property without Income Proof

SBI Loan Against Property Interest Rates

Loan Against Property Eligibility

Bank of Baroda Loan Against Property

Canara Bank Loan Against Property

LIC Loan Against Property

Hero Housing Finance Loan Against Property

Axis Bank Personal Loan Interest Rates

Bajaj Finance Personal Loan Interest Rates

HDFC Personal Loan Interest Rates

ICICI Personal Loan Interest Rates

IDFC FIRST Bank Personal Loan Interest Rates

Kotak Bank Personal Loan Interest Rates

Paytm Personal Loan Interest Rates

PNB Personal Loan Interest Rates

Tata Capital Personal Loan Interest Rates

Bank of Baroda Personal Loan Interest Rates

Blog

HDFC Credit Card Customer Care

Axis Bank Credit Card Customer Care Number

SBI Credit Card Customer Care

AU Bank Credit Card Customer Care Number

American Express Credit Card Customer Care

Standard Chartered Credit Card Customer Care Number

Yes Bank Credit Card Customer Care

IDFC Credit Card Customer Care Number

HSBC Credit Card Customer Care

HDFC Credit Card Airport Lounge Access

SBI Credit Card Airport Lounge Access

Axis Bank Credit Card Airport Lounge Access

HSBC Credit Card Airport Lounge Access

Flipkart Axis Bank Credit Card Lounge Access

Yes Bank Credit Card Lounge Access

Axis Bank My Zone Credit Card Lounge Access

Axis Bank Select Credit Card Lounge Access

Bajaj Finance Personal Loan Customer Care

SBI Personal Loan Customer Care

Indiabulls Personal Loan Customer Care

Kotak Bank Personal Loan Customer Care

HDFC Personal Loan Customer Care

MoneyTap Customer Care

Money View Customer Care

Mpokket Loan Customer Care

Cashe Customer Care

HDB Personal Loan Customer Care

IIFL Personal Loan Customer Care

5 Things to Keep in Mind When Taking a Home Loan

Your home is probably the biggest asset of your life. Not only does it require ample deliberation at your end regarding a wide array of assets such as cost, design, size, location, and so on, but also needs to get a thumbs up from your mortgage lender.

It is only after everything that relates to this property come together, does your dream of owning a home, that you can all you own, can be fulfilled! When we speak of mortgage for your home, you may think of it as a fairly common phenomenon, something that you needn’t think about twice. However, that isn’t the case. In fact, there isn’t just one but numerous aspects that you must know of, before Taking a Home Loan.

Let us take a quick look at each of them!.

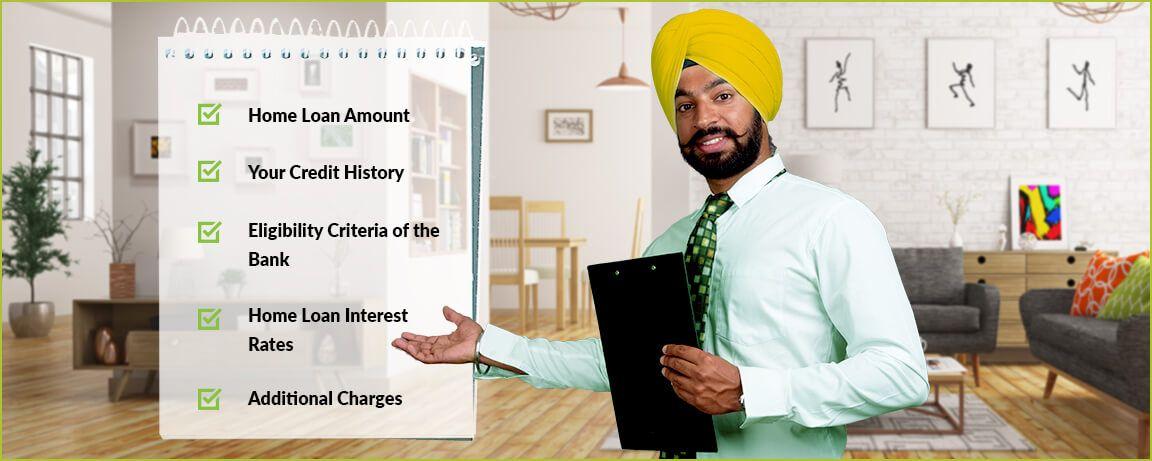

1. Home Loan Amount

There are two factors which play a major role in the determination of the Home Loan amount. One of them is the cost or market value of the home that you are willing to purchase. As a rule of thumb, you ought to pay 20% of the price on your own, and can take the remaining 80% of the value from the bank as a loan. Hence, if your chosen property costs 50 Lakhs, you can expect the bank to offer you a credit worth 40 Lakhs.

However, there is yet another factor that the bank will consider – your ability to repay the loan! In an ideal world, your Home Loan EMI (equated monthly instalment) should not exceed 40% of your total monthly income. Hence, considering you have a salary of 1 Lakh per month and want a loan for 40 Lakhs as discussed above, at a rate of 10.5% for a period of 20 years, the bank may be reluctant to approve your application.

The reason? Your Home Loan EMI is 49,919, much higher than the 40% of 40,000. In such a case, if you want a credit, you may want to have a co-applicant. Considering your spouse is also an earning member, and brings home 80,000 a month, your combined home loan eligibility will enable you to pay an EMI of up to 72,000 thus implying that your Home Loan Application will get swift approval.

If you wish to calculate the ideal Home Loan amount for you, you can do so with the help of MyMoneyMantra’s Home Loan EMI Calculator.

2. Your Credit History

Yet another aspect that plays a crucial role in your Home Loan application process is your credit history. A good credit history indicates a respectable financial discipline on your part. Generally, lenders consider anything above 650 as a good score for a potential Home Loan candidate. A score below that might put a question mark on your creditworthiness and may lead the lender to be a little reluctant about lending you such a hefty amount.

However, there are numerous ways to improve your credit score, one of which is getting a small loan under your name, and paying it off dutifully. You can also get one or more Credit Cards, and remain upfront about your payments to see a steady rise in your credit score. Once your score has reached the optimal level of 650 or above, you will be able to get a Home Loan, rather easily.

3.Eligibility Criteria of the Bank

To safeguard itself from any unsolicited losses, your bank would most likely have some internal criteria in place to gauge your ability as well as willingness to repay the loan. As per these criteria, the bank may usually want you to:

- Be above the age of 21 and below the age of 50

- Have a steady source of income

- Have the minimum possible number of existing loans

- Have a strong repayment history

- Have a decent financial portfolio

While it may not be necessary for you to meet all of these criteria, the more you do, the better will be your chances of getting a quick go ahead on your application.

4. Home Loan Interest Rates

There are two types of Home Loan interest rates:

- Floating interest rates (varying throughout the tenure as per market rates)

- Fixed interest rates (remain fixed throughout the loan tenure)

The former is usually cheaper but puts you at an inconvenience of paying different EMI every month, which may be difficult to manage, especially if you are a salaried individual. Fixed rate Home Loans prove to be comparatively more expensive in the long run, but helps you enjoy the much-needed peace of mind that comes from knowing exactly how much amount do you need to pay for every EMI.

More often than not, Home Loan interest rates in India range from 8.50 to 11.50%. However, some lenders may offer Home Loans at up to 17% interest rate. The rate usually varies depending on numerous factors such as the type of employment, gender, location and market value of the property and type of bank (private, public or corporate), amongst other factors.

5. Additional Charges

When you are looking at a Home Loan agreement, you should watch out for additional charges. These charges usually include:

- Processing Fee

- Administrative Charges

- Legal Fees

- Valuation Fees / Inspection Fees

- Documentation Charges

- Fee for Changing the Terms of the Loan

- Fee for Changing the Loan Tenure

- Copies of Annual Account Statement

- Pre-Payment Charges

- Late Payment Charges

- Recovery Charges in case of Defaults

- Document Retrieval Charges in case of Foreclosure

Considering that there is a wide range of aspects that you need to take into consideration, before applying for a Home Loan, and during the process of procuring the same, we recommend that you seek the assistance of an expert financial advisor at MyMoneyMantra. This simple step will help you in enjoying a holistic view of the deal, thus ensuring that you enjoy a hassle-free home loan approval, disbursal, and repayment.