Hello,

Guest!

Axis Bank MY ZONE Credit Card

Axis Bank SELECT Credit Card

IndianOil Axis Bank Credit Card

Axis Bank Magnus Credit Card

Flipkart Axis Bank Credit Card

Axis Bank Vistara Credit Card

Axis Bank Rewards Credit Card

Axis Bank Vistara Infinite Credit Card

Axis Bank Neo Credit Card

Samsung Axis Bank Signature Credit Card

Axis Bank Aura Credit Card

Axis Bank Kwik Rupay Credit Card

Axis Bank Vistara Signature Credit Card

Axis Bank Privilege Credit Card

Samsung Axis Bank Infinite Credit Card

Axis Bank Reserve Credit Card

Axis Bank Airtel Credit Card

Axis Bank Insta Easy Credit Card

Axis Bank Freecharge Credit Card

Axis Bank Forex Card

Axis Bank Rupay Credit Card

Axis Bank Burgundy Private Credit Card

Axis Bank Credit Card Interest Rates

Axis Bank Credit Card Pin Generation

Axis Bank Credit Card Offers

Axis Bank Credit Card Types

HDFC Freedom Credit Card

HDFC Indian Oil Credit Card

HDFC MoneyBack Credit Card

HDFC Infinia Credit Card

HDFC Diners Club Black Credit Card

HDFC Swiggy Credit Card

HDFC Regalia Credit Card

HDFC Millennia Credit Card

HDFC Business MoneyBack Credit Card

HDFC Regalia Gold Credit Card

HDFC Regalia First Credit Card

HDFC UPI Rupay Credit Card

Paytm HDFC Bank Credit Card

HDFC MoneyBack+ Credit Card

Tata Neu Plus HDFC Bank Credit Card

Shoppers Stop HDFC Bank Credit Card

Flipkart Wholesale HDFC Bank Credit Card

6E Rewards IndiGo Credit Card

HDFC Times Platinum Credit Card

HDFC Bank Corporate Platinum Credit Card

HDFC Rupay Credit Cards

HDFC Forex Cards

HDFC Virtual Credit Card

Best HDFC Credit Cards

Standard Chartered Smart Credit Card

Standard Chartered Manhattan Platinum Credit Card

Standard Chartered Platinum Rewards Credit Card

Standard Chartered EaseMyTrip Credit Card

Standard Chartered Credit Card Login

Standard Chartered Credit Card Customer Care

Standard Chartered Credit Card Bill Payment

Standard Chartered Bank Credit Card Statement

Instant Personal Loan Apps

Personal Loan Interest Rates

Zype Loan

Lendingplate Personal Loan

Unity Small Finance Personal Loan

SBI Personal Loan

HDFC Personal Loan

IDFC Personal Loan

Poonawalla Fincorp Personal Loan

Prefr Personal Loan

KreditBee Personal Loan

SmartCoin Personal Loan

Kotak Personal Loan

Bajaj Finserv Personal Loan

Tata Capital Personal Loan

Yes Bank Personal Loan

L&T Finance Personal Loan

Cashe Personal Loan

FlexiLoans Business Loan

KreditBee Business Loan

Prefr Credit Business Loan

LendingKart Business Loan

Protium Business Loan

IIFL Business Loan

NeoGrowth Business Loan

SBI Business Loan

ICICI Bank Business Loan

Bajaj Finserv Business Loan

HDFC Bank Business Loan

Axis Bank Business Loan

Women Business Loans

Unsecured Business Loans

Working Capital Loan

CGTMSE Scheme

MSME Loan

PSB Loans in 59 Minutes

SBI E Mudra Loan

PMEGP Loan

Mudra Loan

Startup Business Loan

Saksham Yuva Yojana

Pradhan Mantri Rojgar Yojana

PMFME Loan

PM Vishwakarma Yojana

Home Loan Interest Rates

Best Home Loan Interest Rates

HDFC Home Loan

DDA Housing Scheme 2025

PNB Housing Finance

Tata Capital Housing Finance

Aditya Birla Housing Finance

Kotak Mahindra Bank Home Loan

IDFC First Home Loan

Bajaj Finserv Home Loan

5 Crore Home Loan EMI

2 Crore Home Loan EMI

1 Crore Home Loan EMI

70 Lakh Home Loan EMI

Pradhan Mantri Awas Yojana

Hero Housing Finance

Home Loan Balance Transfer Interest Rates

HDFC Home Loan Balance Transfer

Kotak Home Loan Balance Transfer

PNB Home Loan Balance Transfer

Home First Home Loan Balance Transfer

Canara Bank Home Loan Balance Transfer

PNB Housing Finance Home Loan Balance Transfer

Aditya Birla Housing Finance Home Loan Balance Transfer

Loan Against Property Interest Rate

TCHFL Loan Against Property

Muthoot Fincorp Loan Against Property

HDFC Loan Against Property

Federal Bank Loan Against Property

Aditya Birla Housing Finance

Kotak Loan Against Property

IDFC First Loan Against Property

Home First Loan Against Property

SBI Loan Against Property

PNB Housing Loan Against Property

Bajaj Finance Loan Against Property

Loan Against Property without Income Proof

SBI Loan Against Property Interest Rates

Loan Against Property Eligibility

Bank of Baroda Loan Against Property

Canara Bank Loan Against Property

LIC Loan Against Property

Hero Housing Finance Loan Against Property

Axis Bank Personal Loan Interest Rates

Bajaj Finance Personal Loan Interest Rates

HDFC Personal Loan Interest Rates

ICICI Personal Loan Interest Rates

IDFC FIRST Bank Personal Loan Interest Rates

Kotak Bank Personal Loan Interest Rates

Paytm Personal Loan Interest Rates

PNB Personal Loan Interest Rates

Tata Capital Personal Loan Interest Rates

Bank of Baroda Personal Loan Interest Rates

Blog

HDFC Credit Card Customer Care

Axis Bank Credit Card Customer Care Number

SBI Credit Card Customer Care

AU Bank Credit Card Customer Care Number

American Express Credit Card Customer Care

Standard Chartered Credit Card Customer Care Number

Yes Bank Credit Card Customer Care

IDFC Credit Card Customer Care Number

HSBC Credit Card Customer Care

HDFC Credit Card Airport Lounge Access

SBI Credit Card Airport Lounge Access

Axis Bank Credit Card Airport Lounge Access

HSBC Credit Card Airport Lounge Access

Flipkart Axis Bank Credit Card Lounge Access

Yes Bank Credit Card Lounge Access

Axis Bank My Zone Credit Card Lounge Access

Axis Bank Select Credit Card Lounge Access

Bajaj Finance Personal Loan Customer Care

SBI Personal Loan Customer Care

Indiabulls Personal Loan Customer Care

Kotak Bank Personal Loan Customer Care

HDFC Personal Loan Customer Care

MoneyTap Customer Care

Money View Customer Care

Mpokket Loan Customer Care

Cashe Customer Care

HDB Personal Loan Customer Care

IIFL Personal Loan Customer Care

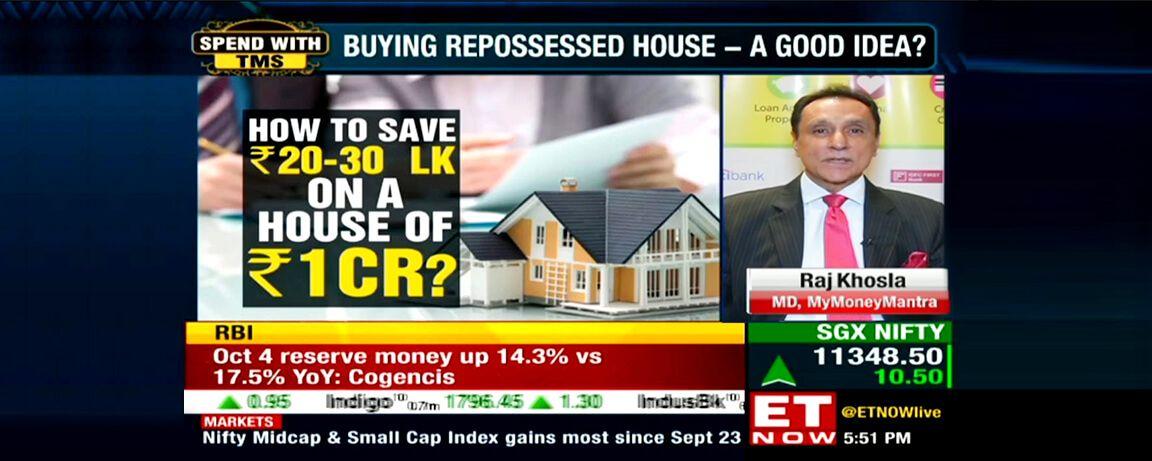

The Money Show with Mr Raj Khosla | Avail Maximum Discounts on Auctioned Homes

Ms Mubina Kapasi of ET Now touch-bases with MyMoneyMantra Founder and Managing Director, Mr Raj Khosla for his expert views on how to derive maximum savings buying a repossessed property under the bank auction for a special edition of the program “The Money Show.”

Here are the excerpts from the interview:

How can one save a few Lakhs worth of Rupees while buying a property that could actually cost you 1 Crore. Well, you can buy a repossessed house on discount and save a huge amount. But what are the Repossessed properties? A repossessed residential property is available for sale at the bank auction. It is essentially a home seized by the bank after the previous owner has defaulted on the payment and lender now seeks to sell the property to recover the money. It could be in the form of auction or public sale. You must have read about such properties on sale in newspaper.

Let’s touch base with the expert, Mr Raj Khosla who is Founder & Managing Director of MyMoneyMantra. Mr Khosla will guide us on how one can process transactions involving repossessed properties and how one can make maximum savings on such deals.

1. Thank you so much for joining us Mr Khosla. To start with, do you think buyers should look at buying repossessed properties? What advantages does it have over buying a regular property?

Mr Khosla:

It is only 5 % of Secured Loan which go bad and therefore eventually end up on the market for re-sale. It is a very low percentage. So we are talking about a low universe to start with.

The biggest advantage is: 20-40% discount on property. Seeing that property prices are already depressed and a further 30 % of discount can end up being a bargain of a lifetime for the buyer.

2. What sort of discount figure on current value one can expect from a repossessed property?

Mr Khosla:

As a rule of thumb, discount figure should be a minimum of 30 per cent of market value. Making a repossessed property a success involves a lot of work and thus I would say, a buyer is entitled to at least “30 per cent” of discount.

3. How can one extract the best value from a purchase of stressed property at the bank auction?

Mr Khosla:

For the sake of simplicity of viewers, let’s take an example of Rs. 1 Crore worth of property, involving typically a 2 bedroom flat that is repossessed. Same rules may apply for warehouses and farm land, but we will discuss a residential unit here.

- First thing you have to do is to figure out your own finances. Before going in for an auction you need to have arranged the money beforehand. You would require money in terms of in-principal loan approval from the bank besides assess the cash you have in hand. You must know how much you can borrow basis your credit rating and other factors. Prior the auction, have a ballpark figure in mind and know how much money you possess.

- Second, is to assess the title of property. Always get hold of a good lawyer for this. Although the bank is auctioning the property under the SARFESI Act but the owner is still the owner and not the bank. So, investigate if the owner has a clear title. Go to central registry and find that. It is very important to ensure that there is no other loan on property. You need to ensure that the owner has not mortgaged the property to some other institution.

- Next get the appraisal of property’s condition done. Whenever one begins to default, chances are high that he tends to not upkeep the house. When someone knows that he is going to lose the property any day in future, the maintenance becomes difficult. It is thus most important to thoroughly appraise the condition of the property. You must know how much more money would be required to actually live in the house after the purchase.

4. Thank you Mr Khosla for highlighting various cautions and precautions involved. But what happens when there are more than two parties involved?

Mr Khosla:

- It will be a tripartite agreement involving the Owner, the bank & the self.

- Try to get the owner as a Confirming Party to this entire agreement. You do not want any niggling property, a legal dispute. You don’t want to buy a problem you want to buy a house.

- Most important, whereby is to get an indemnity certificate from the bank as it will protect you from any legal charges that owner may take as an afterthought.

- Try and put a Penalty Clause. So, in case the owner decides to back off last minute and says he has the cash and wants close the agreement, he is not allowed to make such claim. You have invested money & time and there should not be any possibility for such kind of situation.

- In case there is a society involved, get no objection certificate from housing society. Who knows what litigation the owner may have with the housing society for this the property. So it is important to get an NOC for your own safety.

- If transaction is more than 50 Lakhs, 1 % TDS is deducted & deposited in the permanent account of the owner of the property.

Keep these things in mind. It may sound a bit tedious task, but a lot of people have gained tremendously from such transactions.

- Read auction document “fine print” carefully. Make Lawyer read the document.

- Sometimes you like a property a lot but before you get into auction process, remember you must have an upper limit in mind. Don’t let your emotion let you bid higher than what you have in hand. Always have calculative bids in place. You need to keep your emotions in check all the way through the bidding process.

If you do all of this, you stand to gain a lot. You may end up buying a 3 bed room flat at the cost of 2 bed room flat.

5. What one typically notices is that many of these properties that are auctioned are cornered off by High Net worth individuals as they have links with the banks. Let us understand, do a regular buyer stand a chance at all?

Mr Khosla:

Yes, indeed they do. The steps discussed here should be followed to successfully close a deal at a bank auction for buying a repossessed property. The checklist should be looked upon carefully and this task should be considered as a full time job. May be one may not get it for the first time or the second time, but certainly within 6 to 12 months of constant work in this direction can easily help one land up with a very good repossessed property deal.

6. What care one should take so that they do not end up in a legal tangle?

Mr Khosla:

After following the checklist you are covered from all legal tangles. If at all, there could be only frivolous ones, coming from legal abuse one decides to make and prolong the inevitable.

Indemnity from the bank will be the most important document in such circumstances. The bank has to indemnify you against any such incidences. It covers you for your rights. With indemnity document, you make the bank party for the cover. Make seller the confirming party. It covers you from all bases.

This was an exhaustive explanation around all the things surrounding purchase of repossessed properties, what are the risks involved, and what are the preventions to waive off those risks. Thank you so much Mr Khosla.